What are Life Insurance Ladders?

- Daniel Kurt

- Oct 17, 2025

- 3 min read

Updated: Mar 6

Main takeaways

A life insurance “ladder” means holding multiple term policies with staggered end dates to match your family’s changing needs.

Laddering can save you money compared to buying one large, long-term policy or an expensive permanent policy.

A life insurance ladder gives you more coverage when your dependents need it most, then gradually reduces it as your expenses decline.

Life is all about change. You wince at your Spotify playlist from a few years ago. And those jeans that were so hip once upon a time now seem cringeworthy.

Your financial situation will likely go through twists and turns as well. You may go from a carefree single adult to a parent with multiple kids to support, only to become an empty-nester when they hit adulthood.

Naturally, your life insurance needs will vary over time. So how do you make sure you have the coverage you need, when you need it? That’s where a life insurance ladder can be a smart strategy.

What is a life insurance ‘ladder’?

Building a life insurance ladder involves taking out multiple life insurance policies with different expiration dates in order to obtain the right amount of coverage at any given time. It could mean buying multiple policies at the same time or buying an additional contract at a later date, as your needs evolve.

Typically, a ladder consists of two or more term life insurance policies, which offer a death benefit for a fixed period of time—commonly 10, 20 or 30 years. The big advantage of term policies is that they’re more affordable than permanent policies that protect you for life. Like, a lot more affordable.

By overlapping your coverage during certain years, you’re providing more protection to your family during the years when they need it most. Your financial safety net then gets smaller—as do your total premiums—as each policy expires.

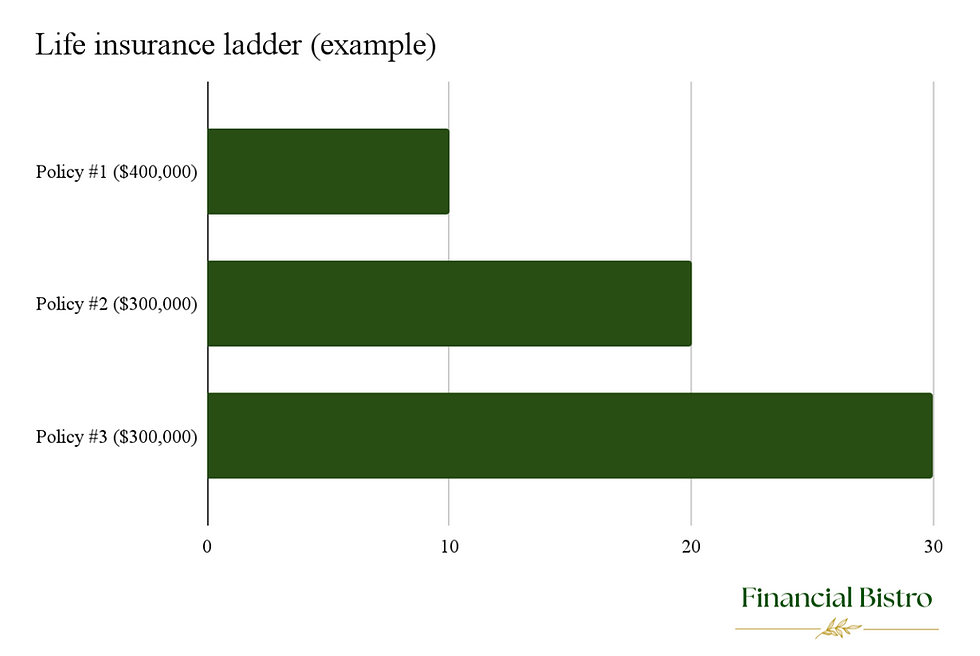

Example of a life insurance ladder

Suppose, for example, that you’re married and about to have a child with your spouse. Assume that your family will require $1 million in coverage to provide for their needs during your child’s first few years. For a 30-year-old male in average health, a 30-year policy of that size would cost in the ballpark of $115 per month.

But your family’s coverage needs will likely decrease as your son or daughter gets older—and even more when they graduate college. So instead of buying a single 30-year policy worth $1 million, you use a ladder strategy with three separate term policies. This involves taking out the following:

You’re getting less protection after Year 10 and after Year 20. But those are periods when your family likely won’t require as much income replacement. The tradeoff is that you’re saving some money in the short-term (you’re paying $97 in premiums in Year 1, instead of $115) and a lot of money in the long-term, when the first two policies expire.

Advantages of life insurance ladders

The main upside to a laddering strategy is that you’re saving money while still getting the coverage you need at any given time. Setting up multiple policies results in lower premiums than taking out one big policy that protects you for a long period of time. And it’s a heck of a lot cheaper than paying for a whole life or other permanent life insurance product, where premiums are several times higher.

Disadvantages of life insurance ladders

One of the disadvantages of a life insurance ladder is that managing multiple policies with different terms and renewal dates can get complicated. You’ll need to stay organized to keep track of when each policy expires and ensure you’re still adequately covered.

It’s also possible to underestimate what your insurance needs will be several years out. If you find that your remaining policies are insufficient, you can apply for additional coverage. But because you’re older at that point, you’ll most likely have to pay a higher premium. And if you’ve experienced any medical issues in the meantime, traditional insurance companies may deny your application altogether.

The upshot

By tailoring coverage through a life insurance ladder, you avoid overpaying for insurance you don’t need later in life. Whenever a policy you own is about to expire, you should reassess your remaining contracts to ensure that your family has the safety net it needs.