The Pros and Cons of Target-date Funds

- Daniel Kurt

- Feb 16

- 5 min read

Updated: Jun 15

Main takeaways

Target-date funds automatically rebalance and get more conservative as retirement approaches.

Different fund managers use different stock/bond mixes and glide paths, so you need to research a particular target-date fund before buying.

While convenient, these funds don’t let you customize your holdings in any way.

Some target-date funds are cheap, but pricier versions can potentially diminish your long-term returns.

Your company’s retirement plan might be one of the most valuable perks of the job. But sorting through the list of investments and choosing where to put your contributions? That can induce a deer-in-the-headlights look.

No wonder, then, that many workers go for the easiest option: a target-date fund that lines up with your retirement timeline. These automated funds represented more than $4 trillion of assets at the end of 2024, according to the investment research firm Morningstar.

While the appeal of target-date funds is undeniable, it’s important to know what they’re actually giving you. Depending on your investment needs and experience level, taking the easy route may or may not be the best way to go.

What are target-date funds?

A target-date fund is an umbrella investment made up of multiple mutual funds, where the holdings automatically shift to less risky assets as the target date draws nearer. Because the asset allocation is done for you, these funds are particularly popular among retirement investors—although they’re also a common option in 529 college saving plans as well.

A 2040 target-date fund, for example, is designed to reflect the risk and reward profile of a typical investor who aims to retire in or around the year 2040. Initially, the fund skews toward growth-oriented stock funds. As the target date draws closer, however, a greater percentage of the asset mix is shifted to more conservative holdings like bond funds or stable value funds.

There are dozens of investment companies that offer their own family of target-date funds, usually with similar-sounding names. But don’t be fooled: Two different funds with the same target date can actually look quite different when you dig a little deeper. One may have a greater portion of stocks to bonds at a given point in time, for example. And one might own a higher concentration of international stocks than the other.

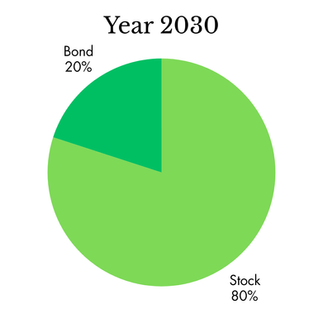

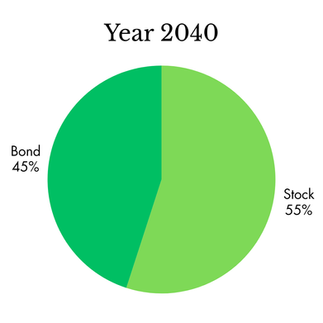

In addition, one target-date fund may have a different timeline for transitioning to more stable assets—known as its “glide path”—than that of a competitor. Below are two hypothetical 2040 target-date funds. One starts with a slighter lower allocation of stock holders and gradually tapers toward a 50/50 split between stocks and bonds at the retirement date. The other initially has a more aggressive allocation, but tapers more dramatically as the fund approaches the target date.

2040 Target-date funds

The pros

Simplicity

Target-date funds are the ultimate “set it and forget it” investment vehicle, which is a major plus if you’re relatively new to investing or simply don’t want to worry about choosing from a complicated menu of individual mutual funds. All the work of choosing funds and maintaining a prudent asset mix is performed for you.

Automatic risk-adjusting

The fund manager shifts assets toward more stable assets as you approach the target date, according to the fund’s designated glide path. So you don’t have to worry about being caught off-guard with an overly aggressive portfolio if the market should experience a downturn right before or after your retirement.

Continuous rebalancing

When you’re managing your own portfolio, it’s easy for your asset mix to get out of whack over time. For example, during a bull market, you may find that the increased stock valuations give you a significantly higher stock allocation than you aimed for. You have to periodically rebalance your assets to keep things in check—selling stocks to buy more bonds, in this case. With a target-date fund, that’s done automatically.

The cons

Lack of control

Perhaps the biggest knock on target-date funds is that you’re giving up control over where you’re investing your money. If you’re morally opposed to a particular company that’s part of an underlying index fund, you’re out of luck. And if you’d like to move toward bonds at a quicker pace than the fund’s glide path? Sorry, Charlie.

That trade-off might be worth it, if ease-of-use is paramount in your mind. But if you want to customize your retirement or college savings strategy in any way, you might want to pick your own investments.

Fees can be higher

Target-date funds charge “acquired fund fees,” which reflect the operating expense of the underlying mutual funds that it holds. Some funds also charge a management fee or a 12b-1 fee—essentially a marketing and sales charge. So you really need to look at the total expense ratio to find out how expensive it is.

Vanguard, for instance, charges just 0.08% in annual expense fees for its 2045 target-date fund, which owns a mix of index funds. But some target-date products—usually those stuffed with actively managed mutual funds—can charge upwards of 1% a year. That’s a huge drag on your returns, and one that few funds justify based on their performance compared to passive options.

Not always tax-efficient

These funds aren’t designed to minimize the tax burden on investors. For example, they have to sell certain assets to maintain their glide path, which triggers capital gains fees. And they generate interest from their bond holdings, which are taxed at your ordinary income tax rate.

That’s not a big deal if you own them in a tax-deferred account like a 401(k) or IRA. But they’re not the most tax-efficient choice if you own shares within a brokerage account.

Harder to tap for emergency needs

When you put money into your retirement account, you probably have every intention of keeping it there until you finally exit the workforce (or at least the full-time workforce). But, alas, life is unpredictable—you never know if you’ll need to tap into those funds to make a mortgage or car loan payment.

Depending on your timing, that can get extra tricky if you have all your long-term savings tied up in target-date funds. Your stock and bond holdings are tied up into a single investment. So during a down market, you’re selling stocks that have seriously diminished in value—never the ideal scenario. If you own stock and bond funds separately, at least you can dip into your more stable assets if you face a financial crisis.

Who should consider a target-date fund?

Target-date funds can be a great pick for your retirement or college savings account if you want diversification and you’re not exactly confident picking individual funds to build your portfolio. At least you’re getting an investment mix that generally suits someone with your time horizon—and you don’t have to rebalance various mutual funds on your own.

But if you’re looking for a little more control over what you own—or your plan only offers pricier target-date funds—you may want to be a little more deliberate about your investment choices.

The upshot

Target-date funds offer a low-maintenance solution, provided you keep them within tax-advantaged accounts like 401(k)s and 529 plans. While they’re a solid choice for novice investors and those seeking simplicity, choosing the right fund requires a careful look at fees and whether the glide path matches your needs.